What would you do if the main breadwinner in your household could no longer bring an Income?

Curve balls. They’re unexpected, often deceptive and it’s impossible to predict their trajectory. That’s why they’re so devastating – in sport and in life.

There’s some interesting data now available about the kind of curve balls that can impact your life, your finances and your retirement.

One in three Australians could be disabled for more than three months before turning 65. If you combine this with another startling fact – that 60% of Australian families with dependents will run out of money if the main breadwinner can no longer bring in an income – you can see the problem. Curve balls are pretty common, but so few people are prepared for them.

With the mortgage to pay, school fees to fund and day-to-day living expenses to meet, you could run down your savings very quickly and face financial difficulty.

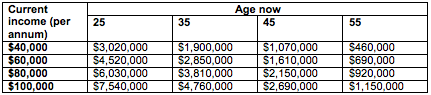

The table below shows what’s at stake in terms of potential earnings to age 65. For example, if you are currently 45 and earn $80,000 per annum, you could earn around $2.15 million over the next 20 years. Isn’t that worth protecting?

Assumptions:

Income increases by 3% per annum. No employment breaks. Figures rounded to nearest $10,000.

What kind of Plan B do you need?

The last thing you need to worry about when you’re dealing with a curve ball is your finances. That’s where insurance comes into its own. It’s a well-known saying that you only realise the value of insurance when you need it – and you don’t have it.

Taking out Income Protection insurance could provide you with a monthly benefit of up to 75% of your income to replace lost earnings while you recover.

Most Income Protection policies offer a range of waiting periods before you start receiving the insurance benefit (with options normally between 14 days and two years). You can also choose from a range of benefit payment periods, with a maximum cover generally available up to age 65.

Other things to consider

· Income Protection insurance premiums will generally be lower if you choose a longer waiting period and shorter benefit payment period.

· If you don’t have sufficient cash flow to fund the Income Protection premiums, you may want to arrange the cover in superannuation, where the cost will be deducted from your account balance.

· Other curve balls you may want to insure for include critical illness (such as cancer and stroke), total and permanent disability and death. These curveballs can be covered by different types of life insurance, which you may want to consider.