When you’re a female juggling a career and a family, you probably feel like you’ve got your hands full. But what if sickness or injury meant you were the one who needed looking after? How much would it cost to replace everything you do – both at work and at home? Getting the right insurance cover is never more important than when others are depending on you.

Sickness and injury can strike at any time. You only have to know someone who’s been struck down by a sickness or accident to know it can, and does, happen.

»»1 in 3 women will be affected by cancer before age 751

»»1 in 4 women will experience depression in their lifetime.

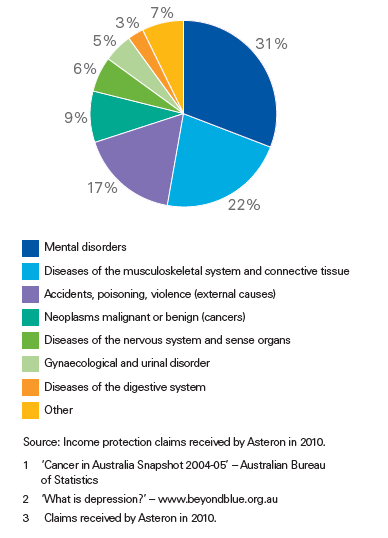

What are the reasons females claim?

1. You can protect your family’s lifestyle by covering against the loss of your income – either on a temporary or permanent basis.

2. You can cover yourself, your spouse, and your children against increased medical expenses.

3. Personal debt protection can ensure your family is not left with unaffordable debt if you can’t work again.

4. Look for policies with flexible features for women – like premium waivers during pregnancy, and the ability to top-up your super while you’re off work.

Strategies for your wallet

1. You can often claim income protection premiums as a tax deduction.

2. You may be able to take out, or top-up, lump sum Life and Total and Permanent Disablement (TPD) cover inside super – potentially reducing the effective cost of cover.

3. If you earn under $61,920 pa and make a voluntary contribution to super, you may be able to use the Government co-contribution to help pay your premiums, and grow your super at the same time.

4. Your may be able to split your spouse’s super contributions to pay your premiums – potentially lowering their tax bill, and reducing the effective cost of cover.

5. You may be able to take out policies for your spouse and/or children, and take advantage of multiple application premium discounts.

Need help? Contact us on 1300 788 650.

Online source: Because you are worth it family – Asteron 2010.