The Coalition Government’s second Federal Budget proposed some important changes, particularly for families, retirees and small business owners.

Budget Snapshot

• Many lower income young families will benefit from greater child care subsidies

• Families choosing not to vaccinate their children will miss out on child care subsidies and family benefits

• Increased Medicare levy low income threshold

• Pension assets test changes will benefit lower net worth retirees, however, higher net worth retirees may receive reduced entitlements

• It will no longer be possible to claim both the full Government and employer provided parental leave payments

• The company tax rate for eligible small businesses will be reduced by 1.5%

• Unincorporated small businesses will receive a 5% tax discount

• Small businesses will be able to fully deduct capital expenses of up to $20,000 per annum

• Tightening of rules on work-related car expense deductions

Your Government Payments – Families

Child Care Subsidy

Proposed date of effect: 1 July 2017

From 1 July 2017, a new Child Care Subsidy will be introduced. This will replace:

• Child Care Benefit

• Child Care Rebate, and

• Jobs, Education and Training Child Care Fee Assistance.

A single means test will apply, subject to an activity test. This subsidised amount is paid directly to the care facility.

The level of support will depend on family income as summarised in the following table.

A new activity test will be established (see table below), with what comprises an activity yet to be announced.

Those families earning less than $65,000 per annum who do not meet the activity test will continue to be entitled to up to

24 subsidised hours per fortnight.

Hourly fee caps, indexed to CPI, will apply. Child care payments will be subject to stronger immunisation requirements.

Paid Parental Leave

Proposed date of effect: 1 July 2016

Currently individuals are able to access both Government Paid Parental Leave, as well as any employer provided parental leave

entitlements. From 1 July 2016, the Government will remove the ability to claim the full amount of both the Government payment and

employer benefits. If the payment from your employer is greater than the Government scheme, which is paid at the minimum wage

for 18 weeks, no Government payment will be available. If your employer payment is less, you can receive a Government top up.

1 Source: http://www.pm.gov.au/media/2015-05-10/jobs-families-child-care-package-delivers-choice-families.

Financial support for families with nannies

Proposed date of effect: 1 January 2016

The Government proposed a two year pilot program to subsidise the cost of child care provided in the family home by nannies, which

will commence on 1 January 2016. The program will extend financial assistance to participating families who:

• have difficulty obtaining child care due to irregular working hours (eg shift workers)

• are in rural or remote areas, or

• have other accessibility issues.

Support will be subject to a fee cap of $7.00 per child per hour.

Care will be provided for up to 50 hours per week, which is the same as the current child care benefit. Families must meet the program

requirements and earn less than $250,000 per annum. The program requirements are yet to be released.

Nannies will need to be attached to an approved service, be 18 years or older, have a current ‘Working with Children’ check and have

first aid qualification. There will be no requirement to hold a minimum early childhood qualification.

Family Tax Benefit – Part A

Proposed dates of effect: 1 January 2016 and 1 July 2016

From 1 January 2016, families will only be eligible to receive Family Tax Benefit – Part A (FTB-A) for six weeks in a 12 month period,

whilst overseas. Currently for temporary overseas absences, the standard rate is payable for the first six weeks which then reduces to

the base rate for a further 50 weeks. The period of time that the standard rate is payable may be extended in special circumstances.

From 1 July 2016, the Government will no longer pay the large family supplement for FTB-A. This supplement is paid for third and

subsequent children and is currently $12.32 per fortnight per child.

Disability support and other pensions

The assets test for all pensions will be changed, effective January 2017. Please see the next section.

Your Government Payments – Retirees

Pension assets test thresholds

Proposed date of effect: 1 January 2017

A number of changes were announced in relation to pension entitlements including:

• changes to the assets test thresholds and taper rate, and

• the removal of the indexation changes announced in the 2014/15 Federal Budget.2

The lower threshold will be increased. However, the taper rate will increase from $1.50 to $3.00 which means the upper (or cut-out

threshold) will reduce. The taper rate is the amount the age pension reduces for every $1,000 of assets over the lower asset threshold.

The tables that show the amount of pension that could be received under these proposed measures can be found in the Minister’s

press release titled ‘Fairer access to a more sustainable pension’.

Note: It’s important to remember that both the income and assets tests are applied. The test which calculates the lowest entitlement determines the age pension payable. The tables in the press release assume entitlement is determined under the assets test only.

Commonwealth Seniors Health Care Card

The Government will ensure age pensioners who lose entitlement due to the above changes will be entitled to the Commonwealth

Seniors Health Care Card (CSHC) from 1 January 2017. The CSHC is designed to assist older Australians by providing a range of

concessions, including:

• discounts on Pharmaceutical Benefits Scheme (PBS) prescription medicines

• bulk-billed doctor appointments (at the doctor’s discretion)

• lower out-of-hospital medical expenses through the Medicare Safety Net, and

• certain state, territory and local government concessions - such as transport or concessions from private business that vary

between each state and territory.

Pension portability

Proposed date of effect: 1 January 2017

The Government permits certain recipients to continue to receive their pension payments while overseas for up to 26 weeks.

However, from 1 January 2017, it is proposed to reduce this time to six weeks. This will apply to pensioners who have lived in Australia

for less than 35 years. Their payments will be paid at a reduced rate proportional to their period of Australian Working Life Residence.

Impacted payments are the Age Pension, Wife Pension, Widow B Pension and Disability Support Pension.

Previous income test proposals

Date of effect: N/A

The Government will not proceed with the income test changes announced in the 2014/15 Federal Budget.

2 Pensions will continue to be indexed to the greater of CPI and Pensioner and Beneficiary Living Cost Index as well as being benchmarked against Male Total Average Weekly Earnings.

Your Business

Company tax rate for small businesses

Proposed date of effect: 1 July 2015

The rate of company tax for eligible small businesses3 will be reduced by 1.5% to 28.5%. These companies will continue to frank their

dividends at up to 30%.

Tax discount for unincorporated small businesses

Proposed date of effect: 1 July 2015

Small businesses that are unincorporated, such as sole traders and partners in partnerships, will be able to reduce their tax liability

related to small business profits by 5%, up to a maximum amount of $1,000.

CGT roll-over relief

Proposed date of effect: 1 July 2016

Small businesses will no longer be subject to Capital Gains Tax (CGT) if it benefits from changing its business structure. For example a

company could be restructured as a trust without the transfer of the company’s assets to the trust triggering CGT.

Accelerated depreciation

Proposed date of effect: 12 May 2015

Small businesses will be able to fully deduct the cost of assets worth up to $20,000 in the year they are acquired. This concession will

be available on purchases from 7.30 pm 12 May 2015 until 30 June 2017. The concession can apply to more than one asset purchased in

the same year.

Drought relief

Date of effect: 1 July 2016

Under a $300 million drought relief package, primary producers will be able to fully deduct capital expenditure on fencing and water

facilities, in the year the costs are incurred. They will also be able to deduct capital expenses related to fodder storage over three years.

3 A small business is defined as a business with an aggregated turnover of less than $2 million.

Your Super

• The only proposed superannuation change of significance is to extend the maximum life expectancy—from 12 to 24 months—

to allow a terminally ill patient access to their superannuation.

• No other new superannuation measures were announced in this year’s Budget, in line with the Government’s 2013 election

commitment to not make changes during its first term.

• In 2015/16, the minimum amount of super contributions employers must make into eligible employees’ accounts under the

Superannuation Guarantee (SG) will remain at 9.5% per annum.

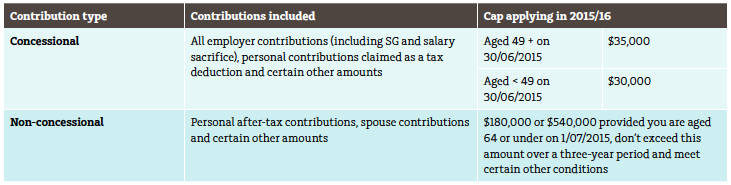

The table below summarises the caps that will apply to super contributions in 2015/16.

Your Tax

• Referred to as the ‘Netflix tax’, it is proposed that GST will be payable on overseas supplied digital products from 1 July 2017.

• Most people who are temporarily in Australia for a working holiday are to be treated as ‘non-residents’ for tax purposes, regardless

of how long they are here. As a result, they will be taxed at 32.5% from the first dollar of income earned.

• A range of tax issues recently raised in a Government Discussion Paper weren’t addressed in the Budget, including a broad based

review of the GST, tax on personal savings and negative gearing.

Your Aged Care

Aged care means testing arrangements

Date of effect: 1 January 2016

If you enter a residential aged care facility from 1 January 2016, any rental income generated by your former home will be assessed

when determining your aged care fees, regardless of how you pay the accommodation costs. Under the existing rules, any rental

income received from your former home is exempt from the means-tested fee if you pay at least part of your accommodation

payment as a daily payment. The change will not impact means-testing for Centrelink or DVA purposes.

Note: The measures outlined in this Federal Budget Summary are proposals only and may or may not be made law.

Any questions???

If you have any questions or to find out more about how the Budget could affect you, please call us on 1300 788 650