Debt can also be used to buy investments with potential to grow in value, like shares and property. This strategy, known as gearing, may help you to build an investment portfolio faster than you otherwise could have.

To help repay the loan, you’ll have income generated by your investments. So, for many people, servicing an investment loan may be an achievable outcome. In this booklet, we outline nine strategies that have the potential to be highly effective in helping people make the most of debt. Individually, each strategy could significantly improve your financial position.

By using a number of them in combination, you could optimise your finances and achieve financial independence sooner.

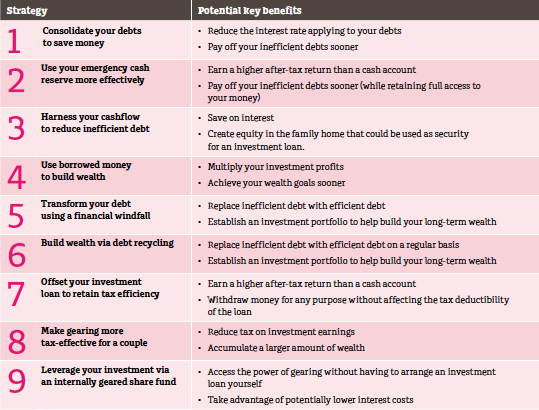

Strategies at a glance:

Tips and traps

• Before consolidating your debts, you should consider whether you need to pay any refinancing costs, including loan application fees, stamp duty and early termination fees. If you have any surplus cash, you should consider using it to reduce personal loans or credit card debt and avoid the need to consolidate your debts.

• Be careful when selecting a fixed rate home loan, as an offset account can usually only be linked to a variable rate loan.

• To accelerate the repayment of inefficient debt, it is essential that you maximise income, limit expenditure and claim all the tax deductions and offsets you are entitled. To help you determine your tax deduction and offsets we recommend you speak to a registered tax agent.

• If you take out a fixed rate investment loan, you can manage interest rate risk and bring forward your tax deduction by pre‑paying up to 12 months interest in advance

• If you have debt, you should ensure you have enough insurance to protect your income and enable the loan to be repaid in the event of your death or disability.

• Arranging a higher investment loan limit could enable you to avoid additional paperwork and fees when adjusting your loan balances each year

• In many cases, the lender will only allow an offset account for the variable rate portion of the loan.

• You should also consider factors such as bankruptcy or litigation when making ownership decisions.

• It’s possible for super funds to borrow to invest in certain assets, provided certain conditions are met.